Apple Pay is widely used by iPhone customers. Businesses considering contactless payments should understand its impact on checkout speed, security and setup requirements.

As mobile wallets become standard at checkout, businesses evaluating digital payment strategies should consider whether Apple Pay belongs in their offering. Consumer expectations around speed, convenience and contactless transactions continue to rise, particularly in mobile-first retail environments.

Apple Pay is Apple's mobile payment platform that enables customers to complete transactions using an iPhone, iPad or Apple Watch. For merchants, accepting Apple Pay can support smoother checkout experiences, enhance payment security and align with broader digital commerce modernization efforts.

However, decision-makers should understand both the operational requirements and strategic implications before enabling it.

Are there drawbacks to implementing Apple Pay?

Not every merchant supports Apple Pay. This problem isn't specific to the Apple service -- Walmart, for example, doesn't accept any contactless payment method besides its own digital wallet, Walmart Pay. For Walmart, this might be a way to encourage the use of its digital wallet and mobile app. For smaller organizations, reluctance to implement Apple Pay and other contactless payment methods might come down to the setup process.

While the setup process is straightforward, it does require organizations to make sure that they have the right technology and, if not, purchase new technology. To accept contactless payments, organizations need to have point-of-sale (POS) terminals with near-field communication (NFC) capability. IT teams must also confirm that their payment processor supports Apple Pay and take steps to meet software and security requirements. Before taking on this process, organizations should make sure that Apple Pay is a good fit for them.

During Apple Pay transactions, vendors don't receive customers' actual card numbers, so they also don't have to deal with sensitive data in their payment systems.

Benefits of using and accepting Apple Pay

Most U.S. retailers accept Apple Pay, but its prevalence isn't the only reason to adopt the contactless technology. When considering why they should accept Apple Pay, organizations can look to customer experience, security and affordable setup.

For retail and digital commerce leaders, the decision to accept Apple Pay typically centers on customer experience, fraud mitigation and checkout optimization.

Mobile payment methods can enhance customer experience

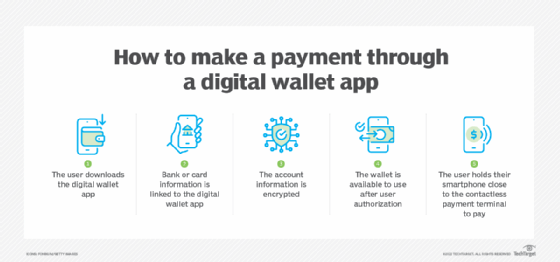

Contactless payment provides a smooth, efficient checkout experience. For users to set up Apple Pay, they should open the Wallet app on their Apple device and add the information for any desired credit, debit or prepaid cards. After that, they can use that device to make payments anywhere that accepts Apple Pay -- online or in-store.

When shopping in person, a customer can simply open the Wallet app on their device, select the card they want to use and hold the device near the NFC card reader for a few seconds to make a payment. When making online or in-app purchases, a customer can choose Apple Pay as the payment method, select the card they want to use and confirm the transaction.

Digital wallet apps such as Apple Pay provide a simple checkout process.

Because of this convenience, Apple Pay is the go-to choice for some users. Whether a customer just prefers the mobile payment option or left their physical wallet at home, accepting Apple Pay can help organizations ensure that the purchase goes through without difficulty.

Apple Pay's encryption system provides strong security

There are also some security benefits that come with using Apple Pay. For customers, Apple Pay ensures secure transactions by requiring user authentication. To authorize a purchase, customers must use their Touch ID, Face ID or passcode. If a user loses their device and has Apple's Find My feature turned on, they can place the device in Lost Mode to suspend Apple Pay rather than having to cancel their cards.

Apple's policy of encrypting card data and tokenizing transactions is helpful for customers and vendors alike. When a user successfully adds a card to Apple Pay, their bank or card issuer will create a device-specific token for it, called a Device Account Number. Apple Pay uses this token to complete transactions, protecting bank account information. The Device Account Number is never stored on Apple servers or backed up to iCloud, and Apple doesn't have access to the original card numbers. This keeps customer data safe and encrypted at every level. During Apple Pay transactions, vendors don't receive customers' actual card numbers, so they also don't have to deal with sensitive data in their payment systems.

Because Apple Pay does not transmit primary account numbers to merchants, it can also reduce breach exposure and simplify PCI compliance scope compared to traditional card processing.

For smaller organizations, reluctance to implement Apple Pay and other contactless payment methods might come down to the setup process.

Setup is affordable and flexible

Apple Pay comes with very few extra costs, if any. As long as an organization doesn't have to get new equipment or switch to a new POS system, there won't be setup fees to accept Apple Pay. When a customer pays with a credit or debit card through Apple Pay, the only merchant fees are those that would already be in place with a regular card transaction. Plus, if a customer pays with Apple Cash from their Wallet app, it's fee-free.

Apple provides other services that businesses can consider in tandem with Apple Pay. When taking the steps to accept Apple Pay, organizations should also look into accepting it as an online payment option on their e-commerce sites. For in-store purchases, some organizations could even implement Tap to Pay to use an iPhone as a payment terminal. This flexibility enables organizations of all sizes to offer a popular payment method to customers with relative ease and minimal costs.

Of course, Apple Pay is only available on Apple devices, and not every customer is an Apple user. Organizations should also offer other contactless payment options, such as Google Pay, to accommodate more of their customer base. Contactless payment methods all rely on the same NFC technology, so it's easy to set up both options.

What business leaders should consider before accepting Apple Pay

Before enabling Apple Pay, leadership teams should look beyond basic setup and consider a few practical questions:

Do your customers expect it? If a significant portion of your customer base uses iPhones, offering Apple Pay can reduce checkout friction.

Will it improve the checkout experience? Faster, contactless payments can shorten lines in stores and simplify online purchases.

Does your current POS system support it? Accepting Apple Pay requires NFC-enabled terminals and payment processor support.

How does it fit into your broader payment strategy? If you offer Apple Pay, you might also want to support other digital wallets to avoid favoring one user group.

What are the security implications? Apple Pay uses tokenization and device authentication, which can limit exposure of card data in merchant systems.

Are there equipment or integration costs? Merchant fees are typically the same as standard card payments, but hardware upgrades might be required.

Editor's note: This article was updated in February 2026 to improve the reader experience.

Katie Fenton is site editor for TechTarget's Mobile Computing, Enterprise Desktop and Virtual Desktop sites.