Mobile payment systems can vary in terms of their fees, setup process and functionality. Organizations must know how to choose the right one to fit their business needs.

There are a few components organizations must account for to provide mobile payment options to customers. Finding a suitable mobile payment system can help simplify setup and management.

Mobile payment systems -- whether through a card reader, all-in-one terminal or smartphone -- make payments quick and easy for consumers. As a result, having systems to collect mobile and online payments should be a top priority for SMB owners and IT admins alike.

However, there are several payment systems to choose from, all with different features, requirements and fees. Organizations must evaluate and compare these factors to make a good decision for their payment system.

Key components of the mobile payment process

It's important to understand that a payment system includes hardware and software. The hardware is the point of sale (POS) system, which runs the software that takes the card information and processes it with the customer's bank. When setting up their payment system, organizations should consider how the POS system, payment system software and payment method factor into the process.

POS system hardware

Most merchants use a POS device that processes customers' credit card information. This can be an all-in-one POS system or a card reader that's connected to a display. Customers are generally able to pay by swiping or inserting their card in the terminal or by tapping their card or smartphone against it.

Additionally, a smartphone or tablet can function as a mobile point-of-sale (mPOS) terminal. Merchants can utilize POS software such as Apple's Tap to Pay feature on their device to set up a simple POS system. Customers can tap their card or smartphone against the mPOS to pay.

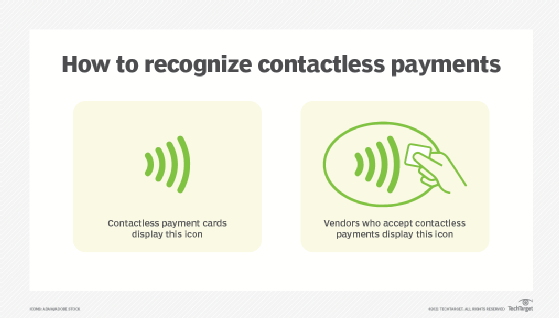

Near-field communication (NFC) is the technology that enables contactless payments. If a card or smartphone features a security token for contactless payment, users can hold it within a few inches of an NFC-capable POS reader in order to make a connection and pay.

NFC-capable POS readers provide a simple payment option for customers who have a mobile wallet or contactless payment card.

Organizations should consider their business requirements when choosing from the following three POS hardware approaches:

All-in-one POS system. This is a more advanced device that is popular with large retail and service establishments. In addition to a display and card reader, this system might include a barcode scanner, cash drawer and receipt printer. Some are even handheld. Organizations must be sure to purchase one with NFC capability to offer contactless payment to customers.

Standalone credit card reader. This device is more mobile and convenient for small, independent retailers. Several vendors offer different sizes and configurations to meet different business needs. This type of reader does not come with a display, so users must connect it to a smartphone or tablet via USB or Bluetooth.

MPOS terminal. This can be the merchant's smartphone or tablet, which eliminates the need to purchase a dedicated POS device. Most modern smartphones feature a built-in NFC reader, so mPOS apps make it possible to use that technology to accept payments from other mobile devices and contactless credit and debit cards. While this is not feasible for large organizations, SMBs and consumers can use this method.

IT decision-makers should determine which POS hardware to use based on pricing, payment methodology and customer demographics. For example, the choice might depend on whether the organization caters more to older customers who typically use plastic credit cards or to younger customers who might prefer digital wallet methods.

Payment system software

Payment system software resides on and interfaces with the POS terminal to take the payment information and process it with the customer's bank for the purchase. It consists of the following components:

POS payment processor. This component sends information between the customer's and merchant's banks and performs other transaction management.

Online payment processor. Online business transactions use a payment processor which processes card payments in the same way that a physical POS terminal would.

Business account. This account enables an SMB to accept funds from customers' credit or debit cards during purchases.

Payment software includes management tools such as inventory tracking, error tracking, custom reporting and customer loyalty programs. Many vendors also offer developer tools such as SDKs and APIs to customize payment methods and extend management tools.

Payment methods

A payment method -- as opposed to a payment system -- is what the customer uses to make a purchase. Historically this has been a credit or debit card. Now, users can store their card information in a digital wallet or app on their smartphone and pay from there. Examples of these electronic payment methods include Apple Pay, Google Pay, Venmo and PayPal. Payment systems must have the right software to enable their use, however. For example, adopting Apple Pay might require an upgrade to the POS system to ensure NFC capability.

Google Pay accepts in-person and offline transactions, including NFC payments and QR code payments.

Apple Pay is available on Apple devices only, while Google Pay works on Android devices. Google Pay can integrate with popular POS systems as well as custom ones using APIs. Like Apple Pay, it requires NFC technology. Google Pay accepts in-person and offline transactions, including NFC payments and QR code payments. There is no fee for Apple Pay or Google Pay.

Mobile payment apps such as Venmo and Zelle run on a computer or smartphone rather than a POS. They enroll the email or phone number of the customer and business via a mobile banking app. Organizations must have a business credit card and business checking account to receive payments. Venmo is also a payment method option with PayPal's online checkout.

There are some drawbacks to these apps, however. They don't provide purchase protection, and many aren't available internationally. Venmo and Zelle are only available to U.S. bank account holders who have a U.S. mobile phone number. Similarly, Cash App is only available in the U.S. and U.K. Although PayPal is available in over 200 countries, its international services come with several fees.

5 mobile payment processing systems to consider

There are some criteria IT admins and business managers should consider when choosing a POS system. Payment system vendors often provide different product options for different kinds of businesses. This way, organizations can choose hardware and software specifically designed to work in retail, dining, sports and other sectors.

First, it's important to determine which type of POS terminal will meet the organization's needs. IT should also evaluate existing POS systems for capabilities such as NFC during this process.

Decide which product offers software features that meet the organization's needs as well. Some cater specifically to restaurants, for example, or have developer tools. Keep the size of the organization in mind, as some products might be a better fit for an SMB than a large enterprise organization, and vice versa.

Additionally, consider the purchasing habits of customers when identifying payment methods and POS devices to use. New technology that will make it easier for customers to pay is often a worthwhile investment.

Organizations should compare the features across different payment processing systems to get a better understanding of their options.

Payment system

Clover

Lightspeed

PayPal

Square

Stripe

All-in-one POS terminal

Yes

Yes

Yes

Yes

Yes

Standalone card reader

Yes

Yes

Yes

Yes

Yes

MPOS capability

Yes

Yes

Yes

Yes

Yes

Online payment processing

Yes

Yes

Yes

Yes

Yes

Android and iOS support

Yes

Yes

Yes

Yes

Yes

E-commerce customization services

Yes

Yes

Yes

Yes

Yes

Business-specific software

Yes

Yes, but limited

Yes, but limited

Yes

No

Custom developer software

Standard libraries

Yes, including custom integrations

Yes

Yes

Yes

24/7 support

Yes

Yes

Yes

No

Yes

Pricing for these products is complicated, as it can include subscription fees and different processing rates based on the type and volume of the transaction. IT decision-makers can delve into these details to weigh out the offerings that will best suit their organization.

The following list was chosen based on comprehensive research into the top payment processing products. This list is not ranked and instead appears in alphabetical order.

Clover

Clover is a POS platform that features custom hardware such as kiosks, cash drawers and a Kitchen Display System for restaurants. Another offering is the Clover Station Duo, a two-screen POS system that provides separate displays for the customer and employee to view. One limitation of Clover is that it has no custom development APIs or SDK. However, it does have some standard API libraries that can enable customization.

Lightspeed

Offering four pricing levels from Starter to Enterprise, Lightspeed is a flexible option for organizations of all sizes. This platform also offers a diverse range of POS systems including barcode readers, printers and a pay-at-table device for restaurants.

PayPal

With a wide array of hardware options, PayPal caters to SMBs by offering customers their first card reader for $29. It also offers customizable POS configurations. As one of the first online payment processing systems, PayPal is a well-established brand, and it checks all the boxes on the other features.

Square

Square is a popular product among SMBs and individual vendors. Merchants can purchase or rent a Square POS terminal or run the app on a tablet. It also offers very low credit card rates and doesn't charge any recurring fees. However, this platform is not ideal for large enterprise organizations because its pricing model favors lower sales volumes.

Stripe

In addition to a wide variety of POS devices, Stripe offers several software development features that cater to enterprise customers. This system also offers some flexibility, as Stripe can run on Lightspeed hardware.

Gary Olsen has worked in the IT industry since 1983 and holds a Master of Science in computer-aided manufacturing from Brigham Young University. He was on Microsoft's Windows 2000 beta support team for Active Directory from 1998 to 2000 and has written two books on Active Directory and numerous technical articles for magazines and websites.