jro-grafik - Fotolia

Don't let blockchain complexity bog down business applications

Enterprise blockchain applications that run in a controlled environment don't require some of the components of cryptocurrency networks, explains expert David Teich.

Along with machine learning and AI, another big buzz technology these days is blockchain. The idea of a distributed data chain first took shape in 2009, when somebody or a group of somebodies using the name Satoshi Nakamoto launched bitcoin and a blockchain network underpinning the cryptocurrency.

Blockchain technologies and usage have both expanded since then, but even supposedly generic blockchain platforms like Ethereum are linked to the concept of passing around digital tokens as a form of virtual currency. The problem with that approach is it adds an unnecessary level of blockchain complexity for many enterprise applications that have no need for a currency.

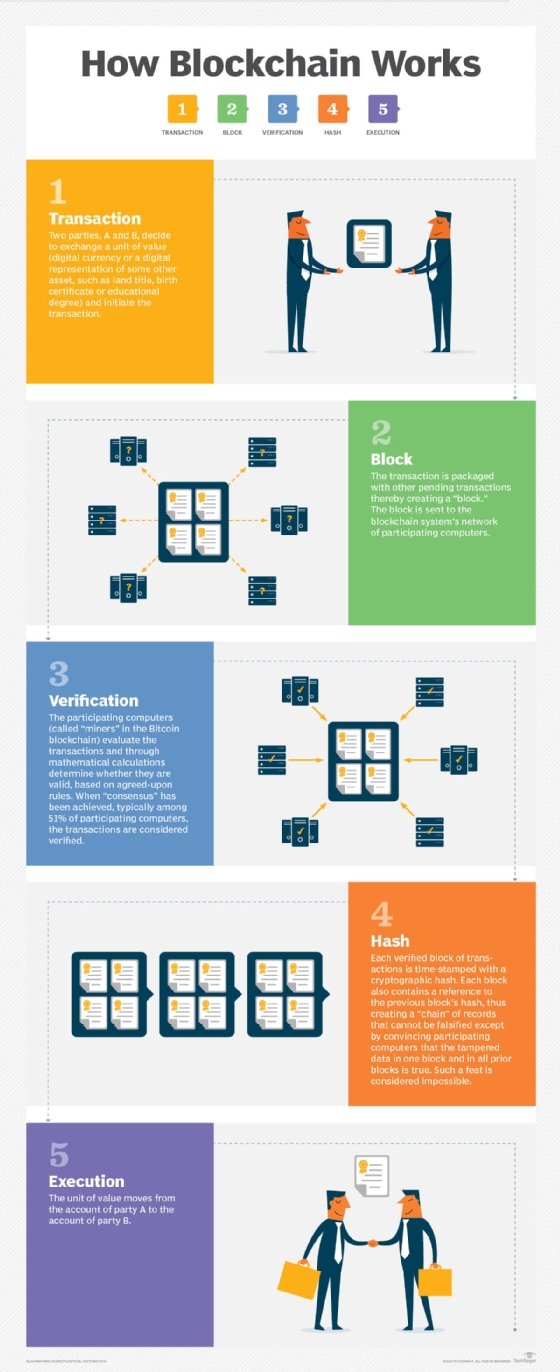

I'll go into more detail about why. But let's start with a generic description of a blockchain. The most basic definition is in the name: It's a chain of blocks of transactions. Other than the capability to distribute the blocks across a peer-to-peer network, blockchains aren't significantly different conceptually than old flat-file systems that required records to be read sequentially.

The power of a distributed blockchain system is that it's more visible to all parties than a database controlled by one party in a transaction. The challenge is that a more open network requires stronger security measures than in on-premises, behind-the-firewall databases. That means cryptography and other security protections are still required, even if the transactions processed on a blockchain network don't directly involve money.

Transaction ledgers: The heart of blockchain

The real key, though, is that a blockchain creates a distributed ledger. It's a history of all the transactions, just as an accounting ledger is for financial payments. And there are some notable differences in how the ledger can be configured for blockchain business applications to avoid bogging down their performance.

One part of the original cryptocurrency version of blockchain is something called consensus. Since cryptocurrency transactions are conducted in the open on the internet, there needs to be a way to verify that the data in a blockchain hasn't been corrupted. Consensus is the idea that a majority of servers in a network approve each transaction before it's executed, so a single actor is less likely to be able to corrupt data.

However, in a narrower enterprise blockchain setting, not everyone on the internet can access the distributed ledger; only trusted players in a controlled group can do so. That means consensus on ledger-changing approvals can be ignored, or at least reduced in scope. In the business world, with limitations on who joins private blockchain networks, the companies that set them up can focus more on managing permissions than on consensus -- thus, easing blockchain complexity.

Another core aspect of cryptocurrency blockchain technology is the smart contract, which is a program that runs on a blockchain network and defines the parameters for an agreement between the parties in a transaction. For instance, a cryptocurrency payment won't be forwarded unless the predefined rules set out in a smart contract are met.

That's a useful element for many applications, particularly the trading of tokens that have monetary or other forms of value. But it's another form of blockchain complexity that often isn't needed for the kinds of transactions processed in business applications.

Take supply chain management, for instance. In conventional IT infrastructures, a manufacturer uses supply chain software to track all the raw materials being fed into the production process. Each company in the supply chain has its own systems, separately tracking the same things as the manufacturer. Reconciling differences in the data in multiple systems can be time-consuming, and opening up databases to business partners is complex.

Blockchain creates one system for all to share

All of that can be done more easily in an enterprise blockchain environment. The manufacturer and its vendors in the supply chain share the same distributed ledger, which means they all see the same thing. There's only one system, so there's far less confusion and no need to reconcile transactions. There's also no need for the processing overhead required by either full consensus or smart contracts.

An SAP pilot project based on the MultiChain open source platform provides an example. The vendor worked with 15 companies in the pharmaceuticals industry to deploy a blockchain network that's used to track and trace prescription drugs as part of efforts to comply with upcoming regulations under the federal Drug Supply Chain Security Act.

"MultiChain is the option that worked best," said Gil Perez, senior vice president of products and innovations and head of digital customer initiatives at SAP. "Smart contracts were not necessary to provide the functionality and performance required by the member companies."

Cryptocurrency can go anywhere and be traded by anyone; that creates performance issues for blockchain networks. On the other hand, as the SAP project shows, enterprise users can utilize the technology's key components in a more efficient manner to support business applications in controlled environments. It's time to break the link between blockchain and cryptocurrency in the business mindset -- and reduce the amount of blockchain complexity that enterprise users face.