Getty Images/iStockphoto

Blockchain: An immutable ledger to replace the database

Blockchains create a secure encryption beneficial to many businesses. This article offers use cases, benefits and limitations of the electronic database.

In the last century, paper lists and ledgers gave way to powerful electronic databases that enable IT admins to search, sort, share and move records and associated information.

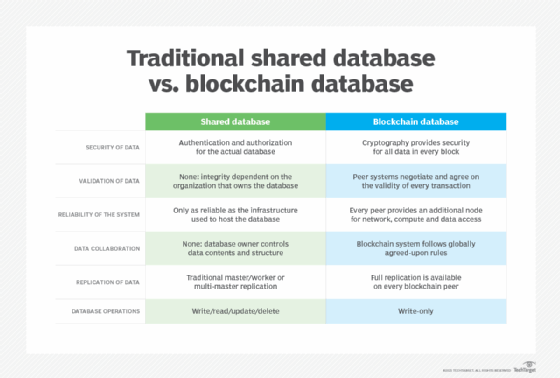

But traditional databases have limitations. For example, databases are singularly owned services. A business deploys, builds and manages its database and the data it contains. The business can then use that data -- or sell or share it with other businesses within its digital economy. The business that owns the database has total control over its design, contents and availability -- and data users are wholly dependent upon the integrity of the data and database owner, often dubbed a "trusted authority." And as the world becomes evermore connected and dependent on data and data sharing, the limitations of traditional databases pose challenges to security and trust.

These limitations have driven the development of distributed electronic database systems. It's a technology intended to democratize information by distributing and synchronizing data between multiple independent stakeholders, such as businesses or governments, that choose to participate in the system. The most common example of this system is blockchain.

What is blockchain?

Introduced in 2009, blockchain is an electronic database, also called an immutable ledger, that holds important information, such as records and ledger entries. But blockchain technology adds features and functions that traditional databases don't have.

First, a blockchain system operates across a peer-to-peer (P2P) network where every network peer shares the computing/networking load and maintains complete copies of the data. As more peers enter the network, the greater system scales up to handle more records traffic. More peers also means greater availability and fault tolerance for the blockchain database.

Second, the contents of an immutable ledger (database) are all related or linked together. Every record, or set of records, added to the ledger represents a block of data. Every block links to the previous block by including a cryptographic hash, a timestamp and transaction metadata. Thus, every block connects to form a growing "chain" of blocks -- deriving the term blockchain -- to create secure and immutable records. A record cannot change without altering the cryptographic hash -- as well as all hashes in subsequent blocks. The combination of cryptography and block interrelationships makes a blockchain database highly secure.

A traditional database can alter records Ad hoc, while a blockchain database can only write data. This is an integral aspect of the security and integrity mechanic: Data can be changed in blockchain, but only by writing a new traceable and auditable block. Consequently, there is never any question about what data was changed, when, why or by whom.

How blockchain works

Blockchain is associated most often with financial transactions -- mainly cryptocurrency transactions such as Bitcoin or Ethereum. As with SQL or any other database format, it can be applied to myriad industry verticals and use cases, not just finance. Let's consider a basic blockchain process.

- A transaction is requested to write a new block of data to the blockchain.

- The request is broadcast to all nodes participating in the blockchain.

- Every node participating in the blockchain checks hashes against algorithms to validate the transaction.

- Every node performs a proof-of-work process, achieves consensus on the validity of the new block and, if consensus succeeds, adds the block to the chain.

For our example, suppose that a business wants to create an immutable, auditable log of server events and errors throughout the enterprise. Each server passes log entries to a common logging server over the network. And each block could contain a series of details, including the following:

- the name and address of the originating server;

- the name and address of the destination or logging server; and

- the error, event and other details of the log entry.

Encryption is at the heart of what makes a block special. Blocks are assigned a cryptographic hash, generated exclusively for its data -- and with the hash for the previous block.

A hash works like a fingerprint for data; it is a sequence of hexadecimal numbers calculated through a mathematical algorithm. This algorithm produces a unique hash (fingerprint) for every block. Change a single bit anywhere in the block and its hash becomes completely different. That block's adjusted hash is also passed to, and recorded with, the subsequent block.

This process creates a series of blocks that are not just related, but inseparable. If a hacker changes one bit, the recorded hash for that block won't match the block's new hash and the blockchain alerts administrators. But it's not just that block's (block A) hash the change affects: The new hash doesn't match the subsequent block's (block B) hash, thereby making block B's hash -- and every subsequent block's (blocks C, D, etc.) hashes -- invalid. This interrelated cryptography makes blockchain databases secure and is the system that enforces immutability.

But the hashes are not enough to ensure complete security on their own. Modern computing power sometimes offers hackers the ability to recalculate and insert new hashes that hide their tampering -- either partially or fully -- in just a matter of minutes.

Blockchain databases delay the creation of blocks deliberately via a time-consuming computational process, performed for every block. The technique is called proof-of-work and requires that computation is performed and validated before a block can join the chain. A typical transaction might require as long as 10 minutes to complete for every block. This means a hacker requires a significant amount of time to tamper with an extensive blockchain. The likelihood of a hacker invading and revalidating an entire blockchain -- without being detected and remediated -- is exceptionally small.

A distributed P2P network also secures an immutable ledger. Every system, or node, that participates in the database hosts a full copy of the blockchain. Every node verifies each block before it adds the block to that node's copy. All participating nodes create a consensus that determines which blocks are valid. If a node determines that a block is invalid or tampered with, the block is rejected. Thus, an attacker who successfully hacks the blockchain on one node will be detected and rejected by the other nodes participating in the blockchain.

Blockchain versions

Blockchain has evolved since its initial introduction to support a wider range of applications and use cases. There are three major iterations of the technology.

- Blockchain 1.0 represents the early introduction of the technology, focused primarily on financial transactions.

- Blockchain 2.0 expands capabilities to support "smart contracts" that replace traditional paper contracts. Small applets within the chain create, validate, monitor and enforce the terms and conditions of an agreement. Such types of blockchain are increasingly used in supply chain management operations where goods are bought, sold and transported.

- Blockchain 3.0 boosts interoperability and scalability to support decentralized applications, dubbed dApps. A dApp runs on the back end across a decentralized P2P network; blockchain is active on the front end to make calls to the dApp running on the back end.

Blockchains can be public, private or partner.

- A public blockchain is available to any business or user, which allows anyone to add a data block to the chain.

- Private blockchains are intended for use within a single organization -- or even more narrowly, for specific teams or personnel -- but the database can usually be viewed by anyone in that organization.

- A partner blockchain supports a group of organizations that share transactions, such as government agencies.

Blockchain use cases

A wide range of industry verticals use blockchain technology to achieve a variety of tasks. Some common examples of blockchain adoption include the following:

- Finance. Financial markets are some of the earliest adopters of blockchain, using the technology for bookkeeping to replace traditional electronic ledgers, cryptocurrency payments and other market transactions and clearing.

- Government. Governments employ blockchain to hold and provide documents such as deeds and public records.

- Supply chain. Markets use blockchain to exchange data, support billing, manage quotas and track the exchange of goods and services.

- Healthcare. The healthcare industry uses blockchain to hold and protect patient data, gather data for analytics, handle healthcare payments and schedule and provide healthcare services.

- Technology. Blockchain use is increasing in technological applications including smart networks, such as those in smart cities. It also gathers and processes data for IoT devices like drones, supports self-driving vehicles, robotics, supercomputers and analytics.

Blockchain benefits

Blockchain technology brings important benefits for businesses and critical business data.

Security. The use of cryptography, immutability and distributed structure means that a blockchain database is virtually immune to hacking, fraud and other malfeasance. Illicit data changes are detected and rejected reliably.

Resilience. Blockchain is a distributed technology: Every node that participates in the database shares a complete copy of the database and contributes consensus to the validation of each node as it changes. Not only does consensus enhance security, but if a node fails or falls under attack -- such as a distributed denial of service -- the remaining nodes continue to function. It is extremely difficult to attack and disable every node.

Faster business. As the common data set is available to all stakeholders with access to the ledger, a blockchain database can often eliminate traditional manual verifications and transaction settlement times that accompany business transactions. This can help to accelerate dramatically some financial and contractual business operations.

Compliance and governance. The immutable and chronological nature of blockchain data can itself be audited to maintain business or industry compliance, as well as serve as a key element of governance across the business.

Transparency. As the need for general trust increases with global business, the visibility and immutability of public blockchain transactions helps to build and ensure trust that data is fair and accurate.

Blockchain limitations

In spite of the benefits, blockchain poses potential limitations inherent in the technology.

Complexity. Blockchain security carries the burden of higher complexity. Consider the number of nodes and copies of the database distributed among business partners and entities around the world: This places an additional burden on networks and processes. Blockchain is a technology suited to only the most security-sensitive or mission-critical database use cases.

Slower transactions. Although a block can contain a significant amount of data, the time required to perform proof-of-work and achieve consensus across all nodes can slow the process of data input. Some nodes prioritize certain types of transactions over others, enabling backlogs that become problematic to resolve.

Energy-inefficient. An increasing complaint about proof-of-work is that the system requires significant power and time to perform proof-of-work across all involved nodes, yet the benefit of all that computing work is almost nonexistent.

Database size. The need to copy and synchronize a blockchain database across nodes makes it challenging for IT pros to bring on and synchronize new nodes in a timely manner. It becomes increasingly difficult to create and maintain blockchains as they grow larger.

Scalability. Blockchains don't scale well, given the slow speed of block addition process, due to proof-of-work operations. Each block can store a finite amount of data, and only a limited number of blocks can attach to the chain in a given time period. This limits the possible size of the blockchain database.

Ultimately, blockchain and immutable ledger technology are unlikely to be a suitable replacement for all enterprise database applications. Business leaders should adopt and deploy database platforms that are best suited to the needs of the business.