Blockchain vs. traditional database: Differences and use cases

Choosing between blockchain and traditional databases -- or using them together -- requires knowing how each one handles data management and the skills needed to make them work.

Blockchain and database technologies have numerous similarities and differences, and they are often compared against each other.

While both blockchain and database technologies focus on storing and managing data, they differ in their architecture and approach. Traditional databases centralize control, with administrators managing access and modifications, while blockchain systems distribute control across a network of participants. Databases also prioritize flexibility and performance optimization, making them a good fit for complex queries and rapid data manipulation. In contrast, blockchain emphasizes the concepts of immutability and trust through cryptographic verification, creating tamper-resistant records that trade some speed for improved security and transparency.

While the two technologies can serve similar purposes and be used together, they work in different ways. Understanding how blockchain and traditional database technologies work is critical to understanding where each technology can best be used in an application deployment or service.

What is a blockchain?

A blockchain is a decentralized, distributed database or ledger that is replicated and synchronized across computers on a network. Since each computer holds a current copy of the ledger, the data isn't vulnerable to a single point of failure. The copies are updated and validated in parallel by every participant.

Blockchain is a type of distributed ledger technology. It is designed to allow the secure recording of data in an immutable ledger, which means the data theoretically can't be tampered with. Data is cryptographically hashed -- that is, converted to strings of characters that can't be easily decoded -- and stored in blocks that are chained together, which is where blockchain gets its name.

Blockchain isn't just used for storing data. It also enables cryptocurrencies such as Bitcoin and Ethereum's Ether. Blockchain technologies are also foundational to Web 3.0 (aka Web3) platforms, which often rely on cryptocurrency and are touted as the building blocks of the next generation of the web. Blockchain enables the decentralized, peer-to-peer network approach that is critical to the operations of Web 3.0 technologies -- among them decentralized finance, non-fungible tokens (NFTs) and distributed applications.

Key blockchain features

Blockchain features include the following:

- Decentralization. Blockchain does not have a single point of control. Instead, network participants collectively maintain the system.

- Immutability. No one can alter or delete data after it has been recorded and confirmed, enabling an immutable ledger.

- Transparency. All blockchain network participants are able to view transactions and verify the blockchain's state.

- Cryptographic security. Blockchain data is secured with cryptographic algorithms.

- Consensus mechanisms. Blockchain transactions are validated with consensus algorithms. The common approaches are proof of stake and proof of work.

What is a database?

A database is software that is used to store and retrieve data.

There are many types of databases, including relational databases, which use rows and columns to organize data. Relational databases commonly rely on SQL to let users query and access data. Among the most widely deployed relational databases are Oracle Database, Microsoft SQL Server and the open source PostgreSQL.

Another common type of database is the NoSQL database, which, rather than being a single technology, can refer to nonrelational document databases and graph databases. Commonly deployed NoSQL databases include Couchbase, MongoDB and Neo4j.

Databases can serve as a system of record for financial transactions, product catalogs, healthcare systems and supply chain management (SCM), among many business uses. Databases are also commonly part of the application stack for applications such as data analytics, ERP, mobile applications and content management systems.

Key database features

Some database features include the following:

- Centralized management. Only database administrators and those given access permissions have administrative control.

- ACID compliance. Many types of databases meet atomicity, consistency, isolation and durability (ACID) compliance.

- Flexible schema design. Many databases enable users to modify data structures and relationships as requirements evolve.

- Advanced querying. Databases support advanced query languages, including SQL.

- Performance optimization. Indexing, caching and query optimization enable fast data access.

Comparing blockchain and database technology

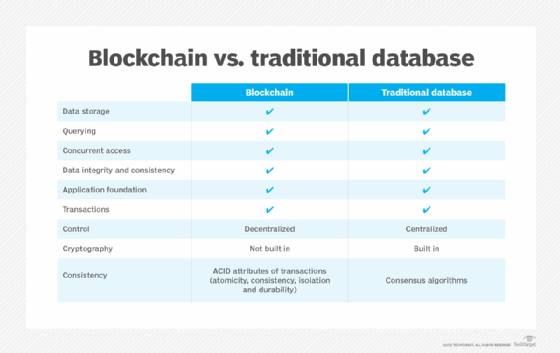

The two technologies share many overlapping capabilities and can be used for some of the same uses. Among the similarities of blockchain and databases are the following:

- Data storage. Both enable users to store information.

- Data queries. The ability to query data is common to both technologies.

- Concurrency. The ability of multiple users to execute queries at the same time is a core feature.

- Integrity and consistency. A hallmark of both technologies is a focus on maintaining data integrity and consistency.

- Powering applications. Applications of all types use both blockchain and databases as a foundation.

- Enabling transactions. Blockchain and database technologies are both commonly used to enable transactions, such as product purchases.

Nevertheless, there are important differences between the typical blockchain deployment and a traditional database. These include the following:

- Control. Most databases are controlled and managed from a central location, while those functions are decentralized and distributed in blockchain.

- Cryptography. While a traditional database can use encryption for security, it's not an integral part of the database or included by default. In contrast, a blockchain, by definition, includes a cryptographic hash. Cryptography is included by default and is what makes the blockchain ledger immutable.

- Consistency. Modern relational databases use four attributes of transactions (ACID), which help to ensure that transactions are executed correctly. With blockchain, consistency comes from the consensus algorithms that synchronize data across the nodes on a chain.

Advantages of using blockchain

Blockchain potentially provides significant advantages to application developers and users, such as the following:

- Web 3.0 integration. Blockchain enables developers to build the decentralized applications that are expected to be a defining aspect of Web 3.0.

- Immutable data. Each transaction in a blockchain is cryptographically hashed to keep it from being tampered with.

- Privacy. Blockchain helps improve privacy by not requiring users to authenticate with anything more than a combination of public and private keys.

- Fault tolerance. The distributed structure of most blockchains minimizes the risk of a single point of failure.

Advantages of using traditional databases

Traditional databases, which have existed for decades, also present many advantages, including the following:

- Familiarity. Developers and users are likely to be far more familiar with deploying and using a traditional database. It is a tried-and-true technology that has stood the test of time.

- Compatibility. Traditional databases are compatible with a massive array of enterprise and consumer applications developed over decades.

- Skills. Traditional database technology has been in use for a long time in critical business processes, and the talent pool of trained database administrators is large.

- SQL queries. SQL provides developers, data analysts and database administrators with an expansive set of capabilities to access, query and manipulate data.

Privacy and security concerns

Blockchain and traditional databases both bring potential privacy and security problems.

Blockchain

Blockchain provides strong security through cryptographic hashing and decentralized architecture, which make it very difficult for someone to tamper with data.

However, the transparency of transactions means that all network participants can view transaction details, and blockchain’s immutable nature prevents easy removal of inadvertently exposed data.

Database

Traditional databases rely on access controls, authentication and role-based permissions for security. They offer granular privacy controls and enable compliance with regulations like GDPR through data deletion capabilities.

However, while centralization enables fast security updates, it also leads to single points of failure. In addition, since databases lack the transparency of blockchain, data could potentially be tampered with or erased without those actions being readily apparent.

Scalability and performance

Some critical differences exist between blockchain and traditional databases when it comes to scalability and performance.

Blockchain

Blockchain brings significant scalability challenges because of consensus mechanisms and distributed architecture. Furthermore, blockchain’s transaction throughput is limited when compared with databases because network consensus creates bottlenecks. Performance optimization requires tradeoffs between decentralization, security and speed.

Database

In contrast, traditional databases are designed for scalability and performance, and they handle thousands to millions of transactions per second through optimization techniques like indexing and caching. They offer multiple types of scaling options, which include advanced monitoring and auto-tuning capabilities.

Industry-specific use cases

Blockchain and databases can serve many of the same industries, though some industry-specific use cases exist for each type of technology.

Blockchain

- SCM. Companies can track food products from farm to store, providing transparency about product origins and handling.

- Financial services. Cross-border payments benefit from blockchain's ability to eliminate intermediaries and maintain an immutable ledger.

- Cryptocurrency. Blockchain is the foundation for building and enabling all cryptocurrencies.

- Healthcare. Secure sharing of patient records and pharmaceutical supply chain verification help combat counterfeit drugs and maintain patient privacy.

- Real estate. Blockchain enables tamper-proof property records and title transfers.

- Gaming and digital assets. NFTs and blockchain-based asset ownership allow players to own and transfer digital items across different games and platforms.

Database

- Healthcare. Database use cases include electronic health records, patient scheduling and medical research data management.

- Financial institutions. Databases enable real-time transaction processing.

- Retail organizations. Databases also enable inventory management, customer relationship management and e-commerce platforms.

- Government agencies. Database use cases include citizen services, tax collection and public safety systems.

- Telecommunications. Database use cases include billing systems, network management and customer service platforms.

Which technology is right for you?

Choosing between blockchain and traditional databases should include consideration of several critical factors.

Think about the trust model. First, consider the trust model of the use case. If a certain use case needs to eliminate intermediaries and create trustless transactions, blockchain might be the appropriate choice. However, if an organization can manage trust through established processes and authorities, a traditional database is likely more efficient.

Evaluate your performance requirements. Traditional databases generally outperform blockchain in transaction speed and data-processing capabilities. If a use case requires high-frequency transactions, complex queries or real-time analytics, databases are usually the best option.

Consider regulatory compliance. Traditional databases make it easier to remain compliant with data privacy regulations like GDPR. Blockchain's immutable nature can conflict with privacy laws that require data removal capabilities.

Evaluate technical expertise and resources. Traditional databases benefit from having experienced administrators on hand and established best practices. Meanwhile, blockchain requires specialized knowledge and is still an emerging technology with evolving standards, which can make it more difficult to bring on the right technical expertise and resources for the organization.

Examine data characteristics. Traditional databases are well suited for dynamic data that includes complex relationships and that requires frequent updates as well as sophisticated querying capabilities. Meanwhile, blockchain works well with append-only data that benefits from immutable records, such as audit trails, certificates and transaction histories.

Hybrid approaches

An emerging trend is the development of somewhat hybrid products. These integrate a form of blockchain, typically as a table type, inside a traditional database.

An increasingly popular approach to database product development is to have a multimodel database. In the multimodel approach, relational, document, graph database and other models -- including blockchain -- are all available in a single database.

Traditional database vendor Oracle, for example, began to integrate blockchain into its multimodel approach with the Oracle Database 21c update released in January 2021. With the Oracle approach, a blockchain table -- an immutable, cryptographically assured set of data stored in table format -- is available. It isn't the same, fully decentralized approach that normally typifies blockchain, but it is blockchain, nonetheless.

Oracle isn't the only traditional database vendor to embrace some of the concepts of blockchain. Microsoft introduced a distributed ledger with blockchain-type functions in its Azure SQL database in May 2021.

Sean Michael Kerner is an IT consultant, technology enthusiast and tinkerer. He has pulled Token Ring, configured NetWare and been known to compile his own Linux kernel. He consults with industry and media organizations on technology issues.