carloscastilla - Fotolia

How blockchain works: An infographic explainer

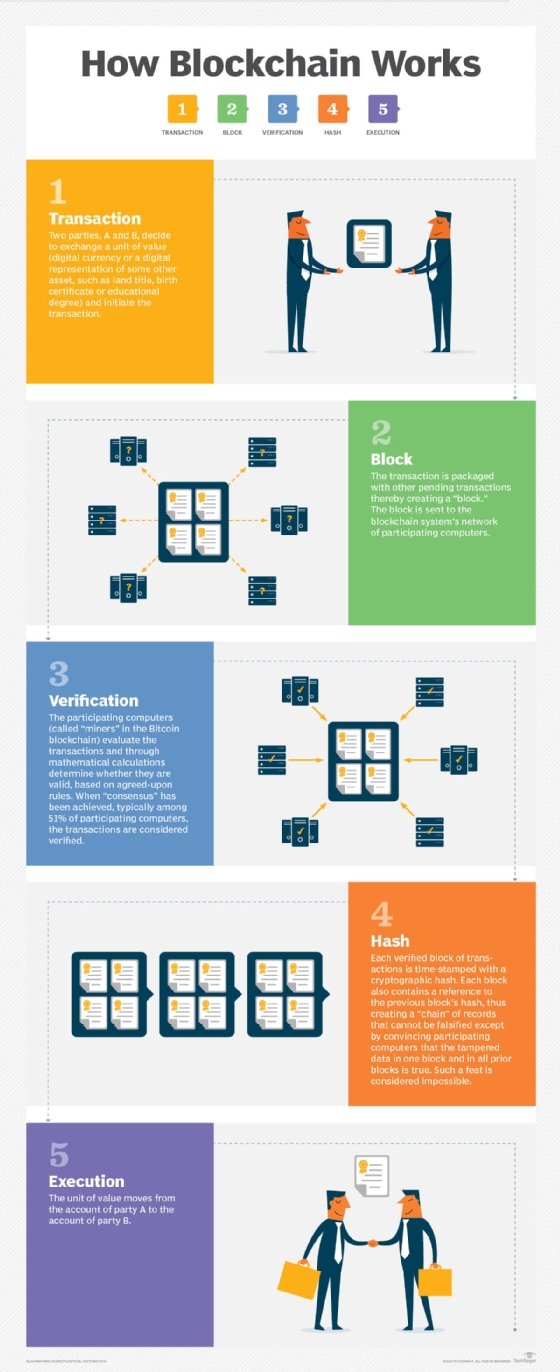

Understanding how a blockchain works is the first step in taking advantage of the technology. Learn how a blockchain unit of value moves from party A to party B.

A blockchain is a type of distributed ledger that uses encryption to store permanent and tamper-proof records of transaction data. The data is stored via a peer-to-peer network using a "consensus" principle to validate each transaction.

One of the major benefits of a blockchain system is that it holds promise to eliminate -- or vastly reduce -- friction and costs in a wide variety of applications, most prominently financial services, because it eliminates a central authority (e.g., a clearing house) in conducting and validating transactions.

Blockchain technology underpins cryptocurrencies -- specifically bitcoin and Ethereum -- and it is being explored as foundational technology for a range of other systems of record like mobile payments, property ownership records and smart contracts.

How blockchain works

To get a solid understanding of how to use blockchain in an enterprise setting, CIOs must first grasp how a unit of value in a transaction moves from party A to party B. This infographic details how blockchain works from transaction initiation, through verification, all the way to delivery.

How to implement blockchain

While blockchain is expected to be first and foremost adopted in financial services, it holds potential for a wide range of vertical industries; for instance, the Office of the National Coordinator for Health Information Technology and NIST recently reviewed proposals for 70 different use cases for blockchain for healthcare. But no matter the industry, for businesses that see potential benefits of blockchain -- whether in cost savings or greater efficiencies in existing processes or in revenue opportunities from a new business line -- there's a rigorous and standard implementation process to follow. In our step-by-step guide, Jeff Garzik, co-founder of blockchain services and software company Bloq, recommends that enterprise CIOs plan for a blockchain implementation in four stages:

- Stage 1: Identify a use case and map a technology plan. Choosing appropriate use cases is critical.

- Stage 2: Create a proof of concept.

- Stage 3: Do a field test involving a limited production run with customer-facing data, then step it up to test with more customer-facing products and data volumes.

- Stage 4: Do a full-volume rollout in production.

Societal impact of blockchain technology

Experts predict that the list of blockchain use cases -- and the technology's impact on society -- will continue to grow. According to Don Tapscott, author, consultant and CEO at The Tapscott Group, blockchain's promise to change how wealth is created across the globe is one of the most significant societal impacts to note.

At the DC Blockchain Summit in Washington, D.C., Tapscott also suggested that blockchain will:

- Enable people living in the developing world, who currently don't have bank accounts, to participate in the digital economy.

- Protect rights to property ownership records.

- Help create a sharing economy based on actual sharing.

- Improve the process of sending money to family members in foreign countries via electronic remittance.

- Help consumers monetize data -- including their own data.

- Reduce the costs of doing business.

- Hold government officials accountable with smart contracts.

In the graphic below, U.S. Rep. David Schweikert (R-Ariz.); Bart Chilton, former chairman of the U.S. Commodity Futures Trading Commission; Carl Lehmann, research manager at 451 Research; and David Furlonger, analyst at Gartner, are each quoted this year speaking on the impact of blockchain.

Digging even deeper

If you're getting up to speed on blockchain, here's a glossary of terms:

- bitcoin: a digital currency that is not backed by any country's central bank or government; traded for goods or services with vendors that accept Bitcoins as payment

- bitcoin mining: the act of processing transactions in the digital currency system; the records of current bitcoin transactions -- identified as blocks -- are added to the record of past transactions, known as the blockchain

- cryptocurrency: a subset of digital currencies; they have no physical representation and use encryption to secure the processes involved in conducting transactions

- digital wallet: a software application, typically for a smartphone, that serves as an electronic version of a physical wallet

- distributed ledger: a database in which portions of the database are stored in multiple physical locations and processing is distributed among multiple database nodes; blockchain systems are referred to as distributed ledgers

- Ethereum: a public blockchain-based distributed computing platform with smart contract functionality; helps execute peer-to-peer contracts using a cryptocurrency called ether

- hash/hashing: the transformation of a string of characters into a usually shorter, fixed-length value or key that represents the original string (similar the creation of a bitly link)

- remittance: a sum of money sent, especially by mail or electronic transfer, in payment for goods or services or as a gift

- smart contract: a computer program that directly controls the transfer of digital currencies or assets between parties under certain conditions; stored on blockchain technology