Top 10 benefits of blockchain for business

Blockchain's unique characteristics address many business issues. Here are 10 important benefits of blockchain and examples of the industries taking advantage of them.

The 2009 launch of Bitcoin moved blockchain from theoretical to real-world use, demonstrating that this digital distributed ledger technology works. Since then, organizations have been testing how they, too, can make blockchain work for them.

Big-name companies, government agencies and nonprofit entities are using blockchain to improve existing processes and enable new business models.

The value of blockchain stems from its ability to share data in a secure way among entities, without any one entity having to take responsibility for safeguarding the data or facilitating the transactions.

"It's a ledger of transactions that have unique characteristics, and those characteristics help address problems in our systems and processes," said Ayman Omar, an associate professor in American University's Department of Information Technology and Analytics and a research fellow at the Kogod Cybersecurity Governance Center.

In fact, blockchain and its characteristics can provide numerous advantages to businesses, whether they're using a public blockchain network or opting for private or permissioned blockchain-based applications.

Experts identify the following as the top blockchain benefits:

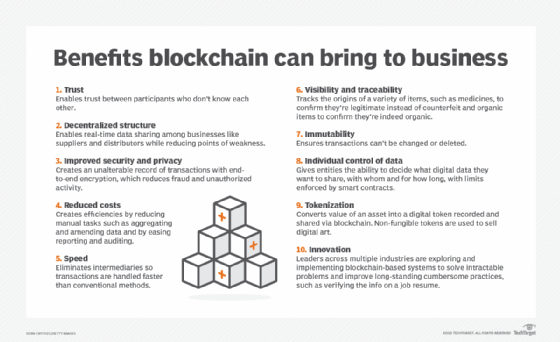

1. Trust

Blockchain creates trust between different entities where trust is either nonexistent or unproven. As a result, these entities are willing to engage in business dealings that involve transactions or data sharing they may not have otherwise done or would have required an intermediary.

Enabling trust is one blockchain's most cited benefits. Its value is evident in early blockchain use cases that facilitated transactions among entities that didn't have direct relationships yet still had to share data or payments. Bitcoin and cryptocurrencies in general are quintessential examples of how blockchain enables trust between participants who don't know each other.

2. Decentralized structure

Blockchain proves its value when there's no central actor who enables trust, said Daniel Field, director of innovation and global head of blockchain at UST, a provider of digital technology and services. In addition to enabling trust among participants who are unknown to each other, blockchain enables data sharing within an ecosystem of businesses where no single entity is exclusively in charge.

Supply chain is an example. Multiple businesses -- from suppliers and transportation companies to producers, distributors and retailers -- want or need information from others in the chain, yet no one is in charge of facilitating all that information sharing. Blockchain, with its decentralized nature, solves that dilemma.

3. Improved security and privacy

The security of blockchain-enabled systems is another leading benefit of the technology. Blockchain creates an unalterable record of transactions with end-to-end encryption to shut out fraud and unauthorized activity. Additionally, data on the blockchain is stored across a network of computers, making it nearly impossible to hack, unlike conventional systems that store one copy of the data on servers. Furthermore, proponents say blockchain can address privacy concerns better than traditional systems by anonymizing data and, in some cases, requiring permission to limit access.

4. Reduced costs

Blockchain's inherent design can also cut costs for organizations. It brings certain efficiencies to transaction processing, reduces manual tasks such as aggregating and amending data, and eases reporting and auditing processes.

Experts like Field pointed to the savings that financial institutions see when using blockchain, explaining that blockchain's ability to streamline clearing and settlement translate directly into cost savings. More broadly, blockchain helps businesses cut costs by eliminating middlemen -- vendors and third-party providers -- that have traditionally handled the processing that blockchain can do. However, some experts assert that blockchain is more expensive than most alternatives, primarily because of the substantial investment in computing resources that it requires.

5. Speed

By eliminating intermediaries and replacing many of the manual processes of transactions, blockchain can handle transactions significantly faster than some conventional methods. However, times can vary, and how quickly a blockchain-based system can process transactions depends on multiple factors, such as network traffic, the size of each block of data and the speed of the process used to establish consensus.

Some experts have concluded that blockchain is faster than other processes and technologies when all the steps – including the manual ones – are taken into account. For example, in one of the most prominent applications of blockchain, Walmart used the technology to trace the source of sliced mangoes in seconds -- a process that previously took seven days.

However, for processes that are already mostly or fully digitized, blockchain is often slower than conventional financial and data-processing systems, according to many experts.

6. Visibility and traceability

Walmart's use of blockchain isn't just about speed. It's also about the ability to trace the origin of mangoes and other products. Blockchain visibility and traceability applications also help retailers manage inventory, respond to problems or questions, and confirm the origin of merchandise.

If a farm recalls its produce because of contamination, a retailer can use blockchain to identify and remove the produce. According to experts, blockchain can help track the origins of a variety of items, such as medicines to confirm that they're legitimate and not counterfeit as well as organic items to confirm they're organic.

7. Immutability

Immutability simply means that transactions, once recorded on a blockchain, can't be changed or deleted. All transactions are time- and date-stamped, so there's a permanent record that can be used to track information over time, enabling secure, reliable auditing of information. Paper-based filing and older computer systems, in contrast, are error prone, and they can be more easily corrupted or retired.

Omar pointed to Sweden's use of blockchain to digitize real estate transactions to keep track of property titles even as they change hands as an example of the benefit of immutability. On the other hand, some observers see immutability as a drawback if, for example, someone wants to remove damaging or inaccurate information.

8. Individual control of data

Blockchain gives individuals unprecedented control over their digital data. "In a world where data is a very valuable commodity, the technology inherently protects the data that belongs to you while allowing you to control it," said Michela Menting, senior research director at ABI Research. Individuals and organizations can decide what pieces of their digital data they want to share and with whom and for how long, with limits enforced by blockchain-based smart contracts.

9. Tokenization

Tokenization is the process whereby the value of a physical or digital asset is converted into a digital token that is then recorded and shared on a blockchain. Tokenization has caught on with digital art and other virtual assets, but it has broader applications that could smooth business transactions, said Joe Davey, a partner at the technology consulting firm West Monroe. Utilities, for example, could use tokenization to trade carbon emission allowances under carbon cap-and-trade programs.

10. Innovation

Leaders across many industries are exploring and implementing blockchain-based systems to solve intractable problems and streamline cumbersome practices. Field cited the use of blockchain to verify the information on job applicant resumes as an example.

The prevalence of resume fraud leaves hiring managers with the time-consuming task of manually verifying the information. But pilot programs that allow participating universities to put data about their graduates and their awarded degrees on a blockchain that can then be accessed by authorized hiring managers helps solve both problems, getting the truth and getting it quickly and efficiently.

Examples of industries that benefit from using blockchain

Blockchain's benefits span industry sectors, but some sectors and enterprises are better suited to the technology than others. Businesses that are decentralized, have multiple parties that need access to the same data, and need a better way to ensure data has not been tampered with have piloted blockchain applications or brought them to full production. The following are a few examples of industries benefiting from blockchain:

- Financial institutions. Their customers are seeing faster and less-costly clearing and settlement.

- Healthcare organizations. Blockchain can secure of patient records and maintain patient privacy while enabling patient data sharing.

- Nonprofits and government agencies. Smart contracts and other blockchain applications help nonprofits create immutable records that enforce stipulated terms.

Disadvantages and challenges

Early implementations of blockchain have exposed some of the technology's disadvantages and challenges as well, experts cautioned.

Blockchain-based applications typically require everyone in a process ecosystem to use blockchain and not some other means of conducting digital transactions. Everyone must invest in the technology and process changes needed to do business on a particular blockchain. Experts noted that many companies don't believe blockchain can deliver high enough returns to justify the cost of replacing existing systems.

Many blockchain systems need support from other systems and processes to verify the accuracy of the data being added. Consider, for example, the use of blockchain for supply chain management. Companies could use such systems to verify suppliers have paid all applicable taxes. But if they're relying on suppliers to confirm that without external confirmation, the value of the blockchain application is weakened because the immutable data on it might be incorrect.

"That's the biggest weakness in blockchain today," Menting said. "It [assumes] all the parties involved adhere to standards, but someone could lie. So there needs to be checks to confirm information. There needs to be some mechanism behind the information to confirm it."

Enterprise uses of blockchain often require some central control despite the technology's generally decentralized nature. "There is still a question about who will address breaches in trust and protocols," Menting said.

'Not a short-term technology'

Given these cautions, business and IT leaders must carefully consider their blockchain investments, according to experts.

They underscored that blockchain's true value comes when it's used in areas where a conventional database won't work and central control and trust aren't present.

"If there's a high level of trust, there's no problem for blockchain to solve. But the more you've got [a] lack of visibility or a potential for corruption, that's where you have bigger use cases. That's where blockchain becomes a solution," Omar said.

He said blockchain-based applications also benefit from being paired with artificial intelligence, machine learning or some other decision-making layer.

Yet experts still believe that blockchain will bring disruption and business transformation, even if the revolution won't happen soon.

"It important to understand that there's been a lot of hype around blockchain. And while it's revolutionary in theory, it's not going to transform society today," Menting said. "Maybe it will 10 to 20 years from now, but it's not a short-term technology."