What is a balanced scorecard and how does the methodology work?

The balanced scorecard is a management system aimed at translating an organization's strategic goals into a set of organizational performance objectives that, in turn, are measured, monitored and changed if necessary to ensure that organizational goals are met.

A key premise of the balanced scorecard approach is that the financial accounting metrics companies traditionally follow to monitor their strategic goals are insufficient to keep companies on track. Financial results shed light on what has happened in the past, not on where the business is or should be headed.

The balanced scorecard system aims to provide a more comprehensive view to stakeholders by complementing financial measures with additional metrics that gauge performance in areas such as customer satisfaction and product innovation.

The business performance management framework was laid out in a 1992 paper published in the Harvard Business Review by Robert S. Kaplan and David P. Norton, who are widely credited with having developed the balanced scorecard system.

Here is how Kaplan and Norton began their 1992 paper:

What you measure is what you get. Senior executives understand that their organization's measurement system strongly affects the behavior of managers and employees. Executives also understand that traditional financial accounting measures, like return on investment (ROI) and earnings per share, can give misleading signals for continuous improvement and innovation -- activities today's competitive environment demands. The traditional financial performance measures worked well for industrial-age companies, but they are out of step with the skills and competencies companies are trying to master today.

Today, the balanced scorecard is widely recognized as a foundational tool in strategic management, allowing organizations to align operations with long-term objectives in a holistic manner.

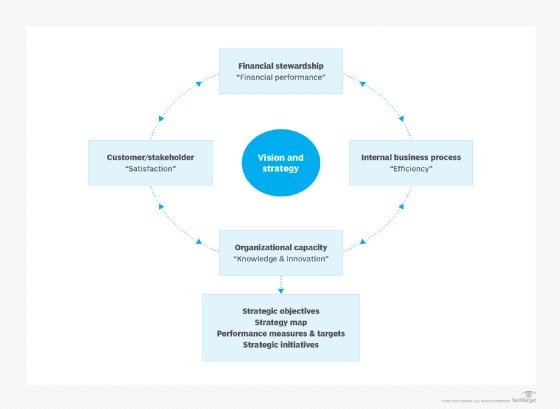

What are the four balanced scorecard perspectives?

The balanced scorecard approach examines performance from four perspectives:

- Financial analysis. This includes measures such as operating income, profitability and ROI.

- Customer analysis. This looks at investment in customer service and retention.

- Internal analysis. This looks at how internal business processes are linked to strategic goals.

- Learning and growth. This perspective assesses employee satisfaction and retention, as well as information systems.

These perspectives are not only interrelated but also mutually reinforcing, providing a multidimensional view of organizational performance.

Why use the balanced scorecard?

Kaplan and Norton cited two main advantages to the four-pronged balanced scorecard approach.

- First, the scorecard brings together disparate elements of a company's competitive agenda in a single report.

- Second, by having all important operational metrics together, managers are forced to consider whether one improvement has been achieved at the expense of another.

"Even the best objective can be achieved badly," the authors stated in their 1992 treatise. Faster time to market, for example, can be achieved by improving the management of new product introductions.

It can also be accomplished, however, by making products that are only incrementally different from the existing ones, thus diminishing the company's competitive advantage in the market long term.

Furthermore, organizations are increasingly using the balanced scorecard as a communication tool to ensure that every employee understands how their daily activities contribute to larger strategic goals.

Emerging trends in balanced scorecards

The balanced scorecard continues to evolve as organizations adapt it to modern business challenges. Recent trends include:

- Integration with technology. Many organizations now implement balanced scorecards through advanced software platforms, enabling real-time data updates and visualization. Tools like Tableau and Power BI allow managers to track key performance indicators (KPIs) dynamically and make swift adjustments when necessary.

- Focus on sustainability. Environmental, social, and governance (ESG) factors are increasingly being incorporated into balanced scorecards. Organizations are adding ESG-specific KPIs to ensure alignment with broader sustainability goals.

- Customization for nonprofits and the public sector. Tailored scorecards are gaining traction in these sectors, addressing unique priorities such as social impact, community engagement, and regulatory compliance.

- Alignment with agile frameworks. The balanced scorecard is being used alongside agile methodologies, enabling organizations to quickly pivot strategies while maintaining long-term objectives.

What are examples of a balanced scorecard?

In their 1993 paper, "Putting the Balanced Scorecard to Work," Kaplan and Norton offered examples of how several companies applied the balanced scorecard, including Rockwater, an underwater engineering firm listed as a wholly-owned subsidiary of Brown & Root/Halliburton; Advanced Micro Devices; and Apple.

The Apple case study is especially interesting in retrospect. According to the authors, Apple (then known as Apple Computer) developed a balanced scorecard to expand the focus of senior management beyond metrics such as gross margin, return on equity and market share.

A small steering committee, versed in the strategic thinking of executive management, chose to include all four scorecard categories and develop measurements within each category.

- From the financial perspective of the scorecard, Apple emphasized shareholder value.

- From the customer perspective, it emphasized market share and customer satisfaction.

- For internal processes, it emphasized core competencies.

- For the innovation and improvement category, it stressed employee attitudes.

Among the highlights of Apple's balanced scorecard planning are the following:

- Apple wanted to shift its classification from a technology and product-focused company to a customer-centric company. Recognizing that it had a diverse customer base, Apple decided to go beyond the standard customer satisfaction metrics available at the time and develop its own independent surveys that tracked key market segments around the world.

- Apple executives wanted employees to focus deeply on a few key competencies, including user-friendly interfaces, powerful software architectures and effective distribution systems.

- Apple wanted to measure employee commitment and alignment with strategic goals. The company deployed comprehensive employee surveys -- as well as more frequent, small surveys of employees selected randomly -- in order to measure how well employees understood the company's strategy and whether or not the results they were asked to deliver by managers were consistent with it.

- Market share was important to senior management, not only for sales growth but also as a factor in attracting and retaining top software developers.

Apple also included shareholder value as a KPI, even though this measure is a result, not a driver of strategic performance, Kaplan and Norton wrote.

Apple's implementation highlights how the balanced scorecard can guide transformation. By prioritizing customer-centricity and innovation, Apple set the foundation for its eventual dominance in the tech industry.

Elements of a balanced scorecard

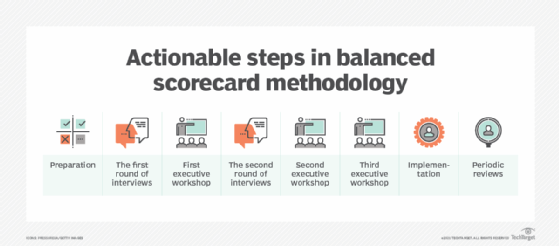

In their 1993 paper, Kaplan and Norton offered guidance on how to build a balanced scorecard. The process they discussed applies to business units and describes what they refer to as "a typical project profile" for developing balanced scorecards.

In brief, here are the eight actionable steps they list:

- Preparation. The organization identifies the business unit for which a top-level scorecard is appropriate. Broadly defined, this is a business unit that has its own customers, distribution channels, production facilities and financial goals.

- The first round of interviews. A balanced scorecard facilitator interviews senior managers for about 90 minutes each to obtain input on strategic goals and performance measures.

- First executive workshop. Top management convenes with the facilitator to start developing the scorecard by reaching a consensus on the mission and strategy and linking the measurements to them. This can include video interviews with shareholders and customers.

- The second round of interviews. The facilitator reviews, consolidates and documents input from the executive workshop and interviews each senior executive to form a tentative balanced scorecard.

- Second executive workshop. Senior management, their subordinates and a larger number of middle managers debate the vision, strategy and the tentative scorecard. Working in groups, they discuss the measures, start to develop an implementation plan and formulate "stretch objectives for each of the proposed measures."

- Third executive workshop. Senior executives reach a consensus on the vision, objectives and measurements hashed out prior in two workshops and develop stretch performance targets for each measure. Once this is complete, the team agrees on an implementation plan.

- Implementation. A newly formed team implements a plan that aims to link performance measures to databases and IT systems, to communicate the balanced scorecard throughout the organization and to encourage the development of second-level metrics for decentralized units.

- Periodic reviews. A quarterly or monthly blue book on the balanced scorecard measures is prepared and viewed by managers. The balanced scorecard metrics are revisited annually as a part of the strategic planning process.

These steps ensure that the balanced scorecard becomes a living document, evolving with the organization's needs and challenges.

History of the balanced scorecard

Kaplan and Norton stressed that the balanced scorecard is not a template to be applied to businesses in general or even industrywide. Businesses must devise customized scorecards to fit their different market situations, product strategies and competitive pressures.

Neither should the balanced scorecard approach be viewed strictly as a performance measurement system.

Rather, it is a strategic management system that will "clarify, simplify and then operationalize the vision at the top of the organization," Kaplan and Norton wrote. How a company's mission statement and vision are operationalized to create value is up to the employees.

"The measures are designed to pull people toward the overall vision," Kaplan and Nolan wrote. "Senior managers may know what the end result should be, but they cannot tell employees exactly how to achieve that result, if only because the conditions in which employees operate are constantly changing."

In the mid-1990s, the scorecard was modified to strengthen the link between performance measures and strategic objectives using a strategy map.

In the late 1990s, the design approach was again tweaked to include the vision or destination statement -- a statement of what strategic success or the strategic end state would look like.

The balanced scorecard approach to management gained popularity worldwide following the 1996 release of Kaplan and Norton's book The Balanced Scorecard: Translating Strategy into Action.

Kaplan subsequently published another book on the subject, called The Balanced Scorecard: You Can't Drive a Car Solely Relying on a Rear View Mirror.

A 2013 brief by Bain & Company, "Management Tools & Trends 2013," lists the balanced scorecard as the fifth most used strategic management tool globally.

Criticism of the balanced scorecard

Criticism of the balanced scorecard method includes charges that Kaplan and Norton failed to cite earlier research on this method and complaints about technical flaws in its methods and designs.

Others have noted that the four perspectives do not reflect important aspects of nonprofit organizations and government agencies -- for example, social dimensions, human resource elements and political issues.

Despite these criticisms, the balanced scorecard remains a widely used tool, with ongoing modifications addressing many of its earlier limitations.

Information technology is a key part of developing an effective strategic plan. Look at these eight free IT strategic planning templates that can help make IT a driving force in a business. Learn how to assess an organization's needs and implement a technology strategy and see how to set business goals in these step-by-step guides. Explore top CIO challenges and how to handle them.