distributed ledger technology (DLT)

What is distributed ledger technology (DLT)?

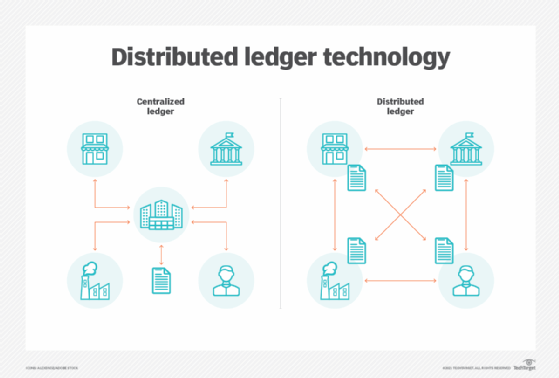

Distributed ledger technology (DLT) is a digital system for recording the transaction of assets in which the transactions and their details are recorded in multiple places at the same time. Unlike traditional databases, distributed ledgers have no central data store or administration functionality.

DLT refers specifically to the technological infrastructure and protocols that enable the simultaneous access, validation and updating of records that characterize distributed ledgers. It works on a computer network spread over multiple entities, locations or nodes.

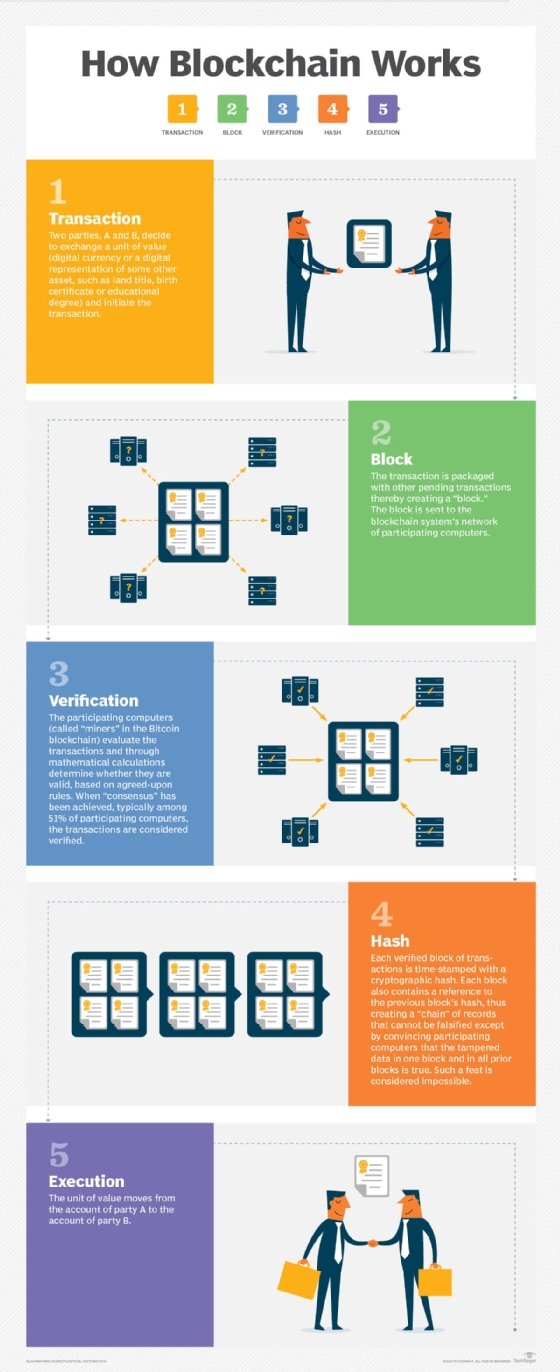

In a distributed ledger, each node processes and verifies every item, thereby generating a record of each item and creating a consensus on its veracity. A distributed ledger can be used to record static data, such as a registry, and dynamic data, such as financial transactions. Blockchain is a well-known example of a distributed ledger technology.

Interest in distributed ledger technology grew significantly in the decade after the 2009 launch of Bitcoin, a cryptocurrency powered by blockchain technology that was the first to demonstrate that the technology not only worked, but could scale and remain secure.

From that time onward, organizations across industries experimented with DLT and how it could be used in enterprise processes. The financial services, healthcare and pharmaceutical sectors were early leaders and supply chain management a common application.

It's important to note that the concept of a distributed ledger is not new. Organizations have long gathered and stored data in multiple locations either on paper or in siloed software, bringing the data together in a centralized database only periodically. A company, for example, might have different bits of data held by each of its divisions, with divisions contributing that data to a centralized ledger only when required. Similarly, multiple organizations working together typically hold their own data and contribute it to a central ledger controlled by an authorized party only when requested or required.

The great advancement of DLT is its ability to minimize or eliminate the often time-consuming and error-prone processes needed to reconcile the different contributions to the ledger, as well as ensure that everyone has access to the current version and its accuracy can be trusted.

How do distributed ledgers work?

DLT works based on principles of decentralization. Unlike traditional centralized databases, DLT operates on a peer-to-peer (P2P) network, where multiple nodes store, validate and update the ledger simultaneously. This eliminates the need for a central authority and reduces the risk of a single point of failure.

The process begins with the replication of digital data across the network of nodes. Each node maintains an identical copy of the ledger and independently processes new update transactions. To ensure consensus, all participating nodes employ a consensus algorithm that determines the correct version of the ledger. Once a consensus is reached, the updated ledger is propagated to all nodes, ensuring synchronization and accuracy.

DLT uses cryptography to securely store data and cryptographic signatures and keys to allow access only to authorized users. The technology also creates an immutable database, which means information, once stored, cannot be deleted and any updates are permanently recorded for posterity.

This architecture represents a significant change in how information is gathered and communicated by moving record-keeping from a single, authoritative location to a decentralized system in which all relevant entities can view and modify the ledger. As a result, all other entities can see who is using and modifying the ledger. This transparency of DLT provides a high level of trust among the participants and practically eliminates the chance of fraudulent activities occurring in the ledger.

As such, DLT removes the need for entities using the ledger to rely on a trusted central authority that controls the ledger or an outside, third-party provider to perform that role and act as a check against manipulation.

Origins of ledgers

Ledgers, which are essentially a record of transactions and similar data, have existed for millennia in paper form. They became digitized with the rise of computers in the late 20th century, although computerized ledgers generally mirrored what once existed on paper.

Ledgers historically have required a central authority to validate the authenticity of the transactions recorded in them. For example, banks need to verify the financial transactions that they process.

Now, 21st-century technology has enabled the next step in record-keeping with cryptography, advanced algorithms, and stronger and near-ubiquitous computational power, making the distributed ledger an increasingly viable form of record-keeping.

This advance comes at a time when such technology is greatly needed. Economic activity has always involved multiple participants, and commerce has almost always crossed multiple jurisdictions and borders. But modern business networks involve an even broader number of participants in more regions, and they have more need to record data for their own uses, as well as satisfy the demands of other participants in their networks. This has stressed conventional ledgers, making them costly to maintain and more vulnerable to errors, computer hacks, manipulation and tampering.

What industries use distributed ledger technology?

The application of DLT spans numerous industries and is revolutionizing several existing processes. The most popular uses of DLT include the following.

Banking and finance

The banking and finance industry has been at the forefront of adopting distributed ledger technology. One notable use case is the implementation of smart contracts in trade finance. Smart contracts facilitate the seamless execution and settlement of trade transactions, reducing inefficiencies and eliminating the need for intermediaries. Additionally, DLT enables faster cross-border payments, enhances Know Your Customer processes and provides secure digital identity solutions.

Supply chain management

Supply chain management is one of the key use cases of DLT. Distributed ledgers help organizations track and verify the movement of goods, ensuring authenticity and preventing fraud. This technology enables real-time visibility into supply chain operations, reduces paperwork and minimizes inefficiencies. For example, a distributed ledger solution can be used to track the provenance of goods, ensuring ethical sourcing and enhancing consumer trust.

Healthcare

DLT is being used to improve patient data management, streamline processes and enhance security. With DLT, medical records can be securely stored and shared, ensuring data privacy and integrity. Additionally, smart contracts can automate insurance claims, reducing administrative burdens and improving efficiency. DLT also enables secure and transparent clinical trials, ensuring the integrity of data and enhancing trust in the research process.

Real estate

DLT has the potential to improve the real estate industry by simplifying property transactions, reducing paperwork and enhancing security. With the implementation of smart contracts, property transfers can be automated, ensuring accurate and tamper-proof records of ownership. Blockchain platforms built on distributed ledgers can provide transparent and auditable property registries, reducing the risk of fraud and disputes and removing the need of costly intermediaries. Furthermore, DLT can enable fractional ownership of real estate, unlocking new investment opportunities and increasing liquidity in the market.

Other industries

DLT also has applications in various other industries. For example, in the energy sector, DLT can facilitate P2P energy trading and enable decentralized renewable energy systems. In the entertainment industry, DLT can revolutionize royalty management and ensure fair compensation for artists. Moreover, DLT has applications in voting systems, intellectual property rights management, gaming and much more.

Examples of distributed ledger technology

Various types of distributed ledger technology are currently in use, including the following:

- Blockchain. Blockchain, which bundles transactions into blocks that are chained together and then broadcasts them to the nodes in the network, is the best-known type of DLT. It powers Bitcoin and other cryptocurrencies.

- Tangle. Tangle, another type of DLT, is geared toward internet of things (IoT) ecosystems. The Eclipse Foundation and IOTA Foundation created the Tangle EE Working Group. Tangle has been described as a "permissionless, feeless, scalable distributed ledger, designed to support trustworthy data and value transfer between humans and machines."

Other well-known distributed ledger technologies include Corda, Ethereum and Hyperledger Fabric.

Why DLT is important

Distributed ledger technology can bring drastic improvements to record-keeping by changing some of the fundamentals of how organizations collect and share the data that goes into their ledgers. To understand this, consider both paper-based and conventional electronic ledgers that require all additions and changes to go through a centralized point of control.

In such a system, organizations must commit significant labor and computing resources to maintain centralized control. Moreover, centralized control means ledgers aren't always complete or up to date. The process is also prone to mistakes and manipulation, as every location that contributes data to the ledger could become a source of fraud or errors.

Additionally, none of the other participants contributing data to the central ledger can efficiently verify the accuracy of data coming from the other contributors. Distributed ledger technology, however, enables real-time data sharing, which means the ledger is always up to date. It also enables transparency, as each participating node can witness those changes. DLT is also more secure by nature because it eliminates the single point of failure and single target for hackers and manipulation that exists with centralized ledgers.

Distributed ledger technology has the potential to speed transactions because it removes the need to go through a central authority or middleman. Similarly, DLT could reduce the cost of transactions. However, running the highly decentralized verification process and distributing copies of the ledger take substantial computing resources, which has been shown to hurt the performance of DLT in certain networking environments compared to centralized ledgers.

Distributed ledger benefits

Much of the early interest in distributed ledger technology has centered on its application in financial transactions. That's understandable, considering that Bitcoin cryptocurrency gained worldwide use, while simultaneously proving that DLT can indeed work. Banks and other financial institutions became early innovators in DLT.

However, DLT proponents say digital ledgers can be used in other industries besides financial services. Government agencies are exploring how to use the technology to record transactions such as real estate title transfers. Healthcare organizations are piloting DLT to facilitate a more efficient way to update patient records. Many businesses are testing DLT for maintaining supply chain data. And the legal profession is looking at how it can use DLT to process and execute legal documents.

Additionally, experts see the technology as enabling individuals to get better control of their personal information by enabling them to selectively share parts of their records when needed and restricting access or limiting the time information is available to other entities. Proponents also say that digital ledgers can help better track intellectual property rights and ownership for art, commodities, music, film and more.

Although DLT adoption is in its early stages, the technology has already shown its ability in many cases to bring benefits to users, including the following:

- Increased visibility into and transparency of data contributed to the ledger.

- Lower operational costs thanks to the elimination of a central authority.

- Faster transaction speeds because there's no lag in updates to ledgers.

- Greatly reduced risks of fraudulent activity, tampering and manipulation.

- Increased reliability and resiliency because there's no longer a central system that creates the potential for a single point of failure.

- Significantly higher levels of security.

Challenges of distributed ledger technology

While DLT has several benefits, it also comes with certain challenges. Some of the most important challenges are the following.

Scalability

DLT systems often face scalability issues as the number of participants and transactions increases. Traditional blockchains have limitations in terms of transaction throughput and confirmation times. However, advancements in technology and the exploration of alternative consensus mechanisms, such as directed acyclic graph (DAG), are addressing these scalability challenges.

Interoperability

Interoperability between different distributed ledger systems is crucial for seamless data exchange and collaboration. However, achieving interoperability remains a complex task due to the lack of standardized protocols and compatibility issues between different DLT platforms. Efforts are underway to develop interoperability solutions and bridge the gap between different networks.

Regulatory and legal frameworks

The regulatory landscape surrounding DLT is still evolving. As DLT disrupts existing systems and introduces new paradigms, regulatory frameworks must adapt in order to ensure consumer protection, privacy and security.

User education and adoption

DLT technologies are relatively new and complex, requiring a certain level of technical knowledge and expertise to fully comprehend and exploit their potential. User education and awareness are crucial for widespread adoption of DLT, and its complexity can sometimes prevent adoption.

Blockchain and DLT: How they relate and differ

The terms distributed ledger technology and blockchain are often used together -- and, sometimes, even interchangeably. They are not the same, however.

Most simply put: Blockchain is a type of DLT, but not all distributed ledger technology uses blockchain technology. This confusion is understandable, given how interest in the technologies jumped after the advent of Bitcoin and how interchangeable the technologies can be in actual use.

Both are used to create decentralized ledgers using cryptography and immutable records that include timestamps. And both are considered nearly unhackable. DLT and blockchain can also be public, making them open for anyone to use, as is the case for Bitcoin, or they can be permissioned (private) and thus restricted to authorized users who agree to certain standards of use.

Now, here's the big difference: Blockchain employs blocks of data that are chained together to create the distributed ledger, just as the name describes. But DLT also includes technologies that use other design principles to create a distributed ledger. To be considered DLT, the technology need not structure its data in blocks.

Distributed ledger technology consensus mechanisms

Consensus mechanisms play a critical role in ensuring the integrity and security of distributed ledger technology. These mechanisms determine how transactions are approved and added to the ledger. Some of the most common consensus mechanisms are the following.

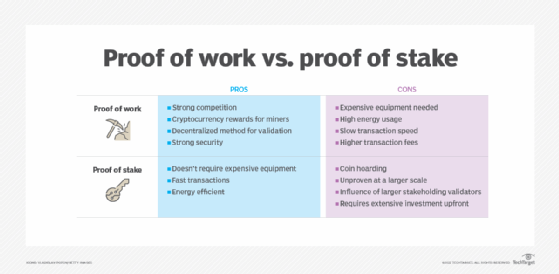

Proof of work

Proof of work (PoW) is the consensus mechanism that underpins the Bitcoin blockchain. In PoW, miners compete to solve complex mathematical problems to validate transactions and create new blocks. This process requires significant computational power, making it resource-intensive and energy-consuming. However, PoW ensures the security and immutability of the blockchain network.

Proof of stake

Proof of stake (PoS) is an alternative consensus mechanism that aims to address the energy consumption and scalability issues associated with PoW. In PoS, validators are chosen to validate transactions based on the number of tokens they hold and are willing to stake as collateral. This mechanism reduces the need for extensive computational power and rewards participants based on their stake in the network. Ethereum is the largest PoS cryptocurrency.

Directed acyclic graph

DAG is a nonlinear data structure that is gaining popularity as a consensus mechanism in distributed ledger technology. Instead of relying on blocks and chains, like traditional blockchains, DAG organizes transactions in a graphlike structure. This enables faster transactions, increased scalability and improved efficiency. Examples of DAG-based cryptocurrencies include IOTA and Hedera Hashgraph.

The future of distributed ledger technology

Whether distributed ledger technology such as blockchain will revolutionize how governments, institutions and industries work is an open question. Experts in this area promote DLT as an important technology that could not only drastically improve existing processes, but could spur innovative new applications. Moreover, they see DLT as part of the "internet of value," where transactions occur in real time across global networks. Indeed, digital ledger technology only exists because the internet that enables it is so pervasive.

However, experts generally believe that adoption of DLT will follow the typical technology curve, with a few leaders out in front, then fast followers and, finally, the laggards. They also note that organizations face challenges in implementing, scaling and operationalizing DLT. To that end, enterprise executives, entrepreneurs and visionaries are now faced with the challenge of establishing the networks of entities that together can take advantage of DLT to radically change how they share and keep records and innovating where DLT can enable entirely new processes and business models.

Blockchain is one of the most popular uses of distributed ledger technology DLT. Learn how to plan the best blockchain deployment with our ultimate enterprise guide.

Continue Reading About distributed ledger technology (DLT)

Dig Deeper on Risk management and governance

-

![]()

Global payments network Swift builds blockchain capability

By: Karl Flinders

-

![]()

What is blockchain? Definition, examples and how it works

By: Kinza Yasar

-

![]()

4 distributed ledger technology risks and how to solve them

By: Bob Reselman

-

![]()

Know how and when to use blockchain vs. distributed ledgers

By: Bob Reselman